Company Background and Competition

Founded in 2013 by Dan Shugar, NEXTracker provides advanced solar tracking technology that rotates photovoltaic panels throughout the day to follow the sun's path across the sky. This tracking capability increases energy capture by 20 to 25% compared to fixed-tilt solar installations, making it a critical technology for utility-scale solar farms seeking to maximize output per acre. NEXTracker went public through an IPO in 2023, increasing efforts to advance solar energy capabilities.

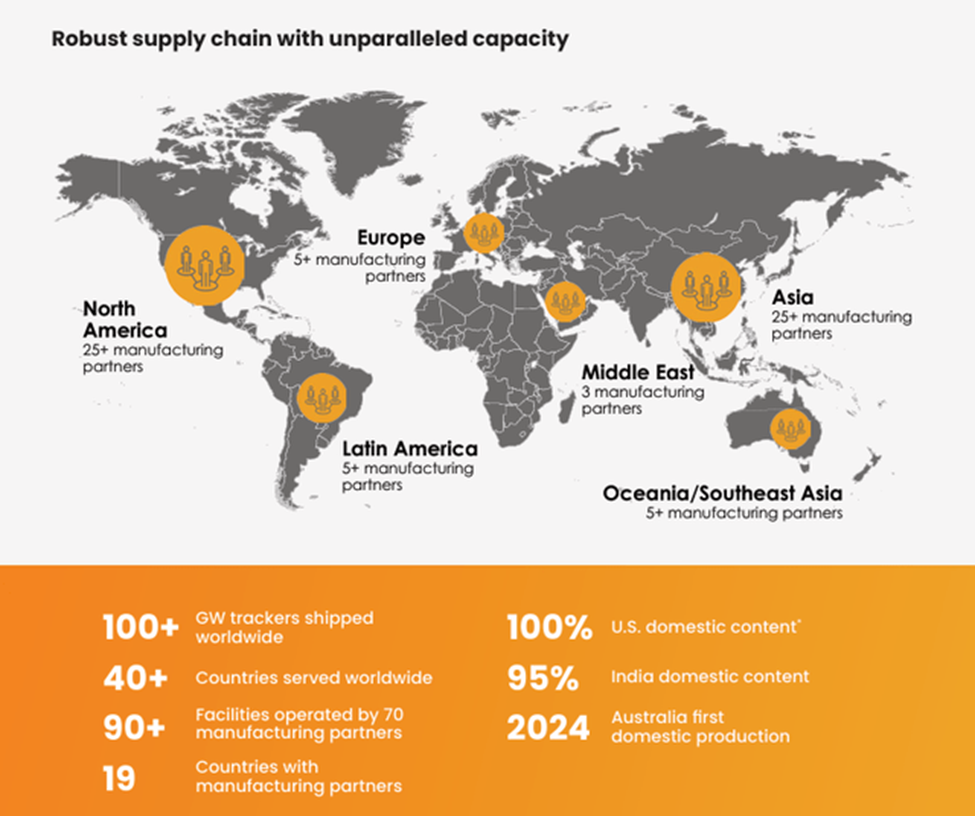

The company has over 25 manufacturing locations within the U.S., with facilities in India, Europe, Australia, and Latin America. The business has seen serious revenue growth over the last three years with a CAGR of 30%.

From 2013 through 2023, NEXTracker has maintained industry leadership with a global market share of 23%, while its closest competitor, Array Technologies, has a market share of 16%. The comparison in FY24 is stark:

NEXTracker vs. Array Technologies — FY2024

| Metric | NEXTracker | Array Technologies |

|---|---|---|

| FY24 Revenue | $2.5B | $1.0B |

| Net Income / (Loss) | $496M | ($240M) |

| Debt-to-Equity | 15% | 574% |

| Times Interest Earned | 42x | N/A |

Global PV Tracker Market Share by Shipments, 2023

Revisiting the Inflation Reduction Act

Like First Solar, NEXTracker has benefited from the Inflation Reduction Act (IRA) and carries similar risks: sensitivity to changes in governmental policy and potential reduction in IRA tax credits. I have previously argued that any revision to the IRA is unlikely to cut tax benefits for the solar industry significantly, if at all.

Boom or Bottleneck? NEXTracker's $8B Backlog Challenge

Solar is a high-growth industry, and several companies have entered the space in which NEXTracker operates. This has led to increased competition. Although the company has successfully maintained its status as an industry leader, it must continue driving innovative technologies into the market and manage its growing backlog.

NEXTracker has a backlog of $4.5 billion, and management forecasts an 80% increase to $8 billion over the next eight quarters. Although backlogs provide insight into the future and signal robust growth, they also create risks:

- With high consumer demand, NEXTracker must be able to meet consumer demands quickly, ensuring customers are satisfied.

- Management must ensure production is efficient and costs are not rising; production disruption could threaten the company's ability to fulfill its backlogs.

To mitigate these risks, the company's management has continued expanding partnerships, material sourcing, and manufacturing facilities globally, tying facility location to demand.

Prepared for a Solar Boom: NEXTracker's Global Expansion

NEXTracker's strong leadership has been capitalizing on increased solar demand worldwide. Notable growth markets:

- India: Solar industry expected to experience a CAGR of 15% over the next 5 years. NEXTracker's India orders include raw materials that are locally sourced and used in entirely local manufacturing facilities.

- Canada: Expected CAGR of 23% over the next 5 years. NEXTracker is the dominant solar tracking technology supplier in Canada.

These are just a few examples of NEXTracker's significant operations and partnerships spanning five of the seven continents.

Acquisitions and Cost-Cutting: NEXTracker's Strategy for Continued Dominance

NEXTracker has maintained market dominance through significant R&D spending and strategic acquisitions. In 2024, NEXTracker acquired two companies:

- Ojjo: Developed specialized technology that makes installing steel pipe foundations more efficient, with less drilling required on hard, rocky terrain. Expects a cheaper, more efficient installation process.

- Solar Pile International: Developed specialized piling technology, including special steel beams that allow solar farms to be solidly built on weakened soil or terrain.

These acquisitions were pursued to cut costs, gain access to specialized technologies, and decrease limitations when building on unreliable terrain.

Cashing In on the Sun: Why I See NEXTracker at $70

With a strong global market presence and proprietary technology, NEXTracker stands to benefit significantly from increased solar energy demand. Due to the company's industry dominance, strong global positioning, and rapid growth, I am placing a $70 price target, signaling 40% upside from current levels of $50 per share.

NEXTracker — Valuation Summary

| Valuation Model | Implied Value |

|---|---|

| DCF (10% CAGR, 3% LTGR, 13.14% WACC) | $67/share |

| P/E Multiple (First Solar peer) | $66/share |

Both models converge around $66–$67/share, strongly supporting the $70 price target.

| WACC | ||||||

|---|---|---|---|---|---|---|

| $67 | 11.14% | 12.14% | 13.14% | 14.14% | 15.14% | |

| LTGR | 2.0% | $79 | $70 | $62 | $56 | $51 |

| 2.5% | $83 | $73 | $65 | $58 | $52 | |

| 3.0% | $88 | $76 | $67 | $60 | $54 | |

| 3.5% | $93 | $80 | $70 | $62 | $56 | |

| 4.0% | $98 | $84 | $74 | $65 | $58 | |

Risks

- IRA policy risk: NEXTracker benefits significantly from Inflation Reduction Act tax credits. Any revision or accelerated phase-out of solar incentives would directly impact the economics of new solar installations and reduce demand for tracking systems.

- Competition intensifying: Array Technologies, GameChange, and other tracker manufacturers are gaining share. As the solar tracking market matures, pricing pressure could compress margins.

- Backlog execution risk: A $4.5 billion backlog growing to $8 billion creates significant fulfillment pressure. Delays in manufacturing, logistics, or installation could lead to customer dissatisfaction and contract cancellations.

- Supply chain concentration: Dependence on steel, aluminum, and specialized components exposes NEXTracker to commodity price volatility and potential supply disruptions.

- Customer concentration: Utility-scale solar projects are large, meaning a relatively small number of major customers can drive a significant portion of revenue. Losing a key customer relationship could materially impact results.

Conclusion

NEXTracker's 23% global market share, 30% revenue CAGR, and $4.5 billion backlog position the company as the clear leader in solar tracking technology. With strong financials, a rapidly expanding global supply chain, and strategic acquisitions that reduce installation costs, I view NEXTracker as well-positioned for continued growth and assign a Buy rating with a $70 price target. I will continue monitoring backlog conversion rates, competitive dynamics, and IRA policy developments.

Equity Researcher · CFA Research Challenge Champion

Independent equity researcher focused on fundamental analysis and long-term value creation. Data-driven, fundamental-first.