An Intro to Airlines and Headwinds

Airlines are essential to global travel, but does that make them vital to your portfolio? I would argue otherwise. Legendary investor Warren Buffett has a history of investing in airline stocks only to regret this decision quickly. After learning from his mistakes, Buffett has notoriously scrutinized airlines as an investment, placing them under a negative spotlight with bold statements such as:

"I have an 800 freephone number now that I call if I get the urge to buy an airline stock. I call at two in the morning and I say: 'My name is Warren and I'm an aeroholic.' And then they talk me down."

Companies such as Delta Air Lines (DAL), United Airlines (UAL), Southwest Airlines (LUV), and American Airlines (AAL) are plagued by structural headwinds, including high fixed costs, razor-thin margins, extreme economic sensitivity, commoditized services, and debt-heavy balance sheets. As a result, airlines often struggle to deliver strong, consistent returns. In fact, the S&P 500 has consistently outperformed airline returns over the long run.

Airline Stocks vs. the S&P 500 — Annualized Returns

| Years | DAL | UAL | LUV | AAL | Mean | S&P 500 |

|---|---|---|---|---|---|---|

| 5 yr | 11.99% | 18.08% | 0.66% | -2.68% | 7.01% | 13.78% |

| 10 yr | 2.90% | 4.13% | 1.17% | -11.34% | -0.78% | 11.10% |

| 15 yr | 10.92% | 9.43% | 8.56% | 2.29% | 7.80% | 12.35% |

| 20 yr | — | — | 5.20% | — | 5.20% | 8.34% |

| 25 yr | — | — | 4.57% | — | 4.57% | 5.78% |

| 30 yr | — | — | 7.28% | — | 7.28% | 9.01% |

High Fixed Costs and Slim Margins Leave Little Room for Error

Due to the nature of the airline industry, carriers operate with substantial fixed costs. These include the ownership and leasing of aircraft, ground equipment, and salary expenses. Combined with weak pricing power, where ticket prices are often dictated by market competition rather than pricing strength, airlines tend to generate consistently low margins.

Based on my analysis of the big four domestic carriers (Delta, United, Southwest, and American) using FY2024 data, the average operating margin hovers around 6%, with net profit margins just above 3.5%. With margins this thin, these companies have limited flexibility to return capital to shareholders or absorb economic shocks comfortably.

Airline Profitability Ratios

| Metric | DAL | UAL | LUV | AAL | Mean |

|---|---|---|---|---|---|

| Operating Margin | 9.73% | 8.93% | 1.17% | 4.82% | 6.16% |

| Net Profit Margin | 5.61% | 5.52% | 1.69% | 1.56% | 3.59% |

Low Differentiation, Economic Sensitivity, and Bailout Dependency

While each carrier offers its version of a customer loyalty program and has expanded premium cabin offerings in recent years, these differentiators have not been strong enough to fundamentally change the industry's pricing dynamics. Premium cabins generate higher margins per seat, but economy class still accounts for the majority of total revenue across domestic carriers. As a result, intense competition on the economy side continues to pressure overall profitability.

With narrow profitability, a slight decline in sales can quickly lead to downward revisions in earnings. During periods of economic turmoil, discretionary spending slows significantly, and travel is often the first category slashed. This not only causes revenue to decline but also places additional pressure on margins, given the industry's high fixed costs.

In addition, many airlines carry heavy debt loads relative to the cash on their balance sheet. Their ability to service this debt is highly dependent on steady earnings, which become especially uncertain during economic downturns.

Often, airlines have relied on government bailouts to survive financial crises. Government support can keep otherwise failing competitors alive, further intensifying competition and depressing pricing power across the industry. This dynamic makes it difficult for any one carrier to gain enough market share to justify higher ticket prices.

The situation raises an important question for long-term investors: Why invest in a business that cannot withstand a downturn without government support?

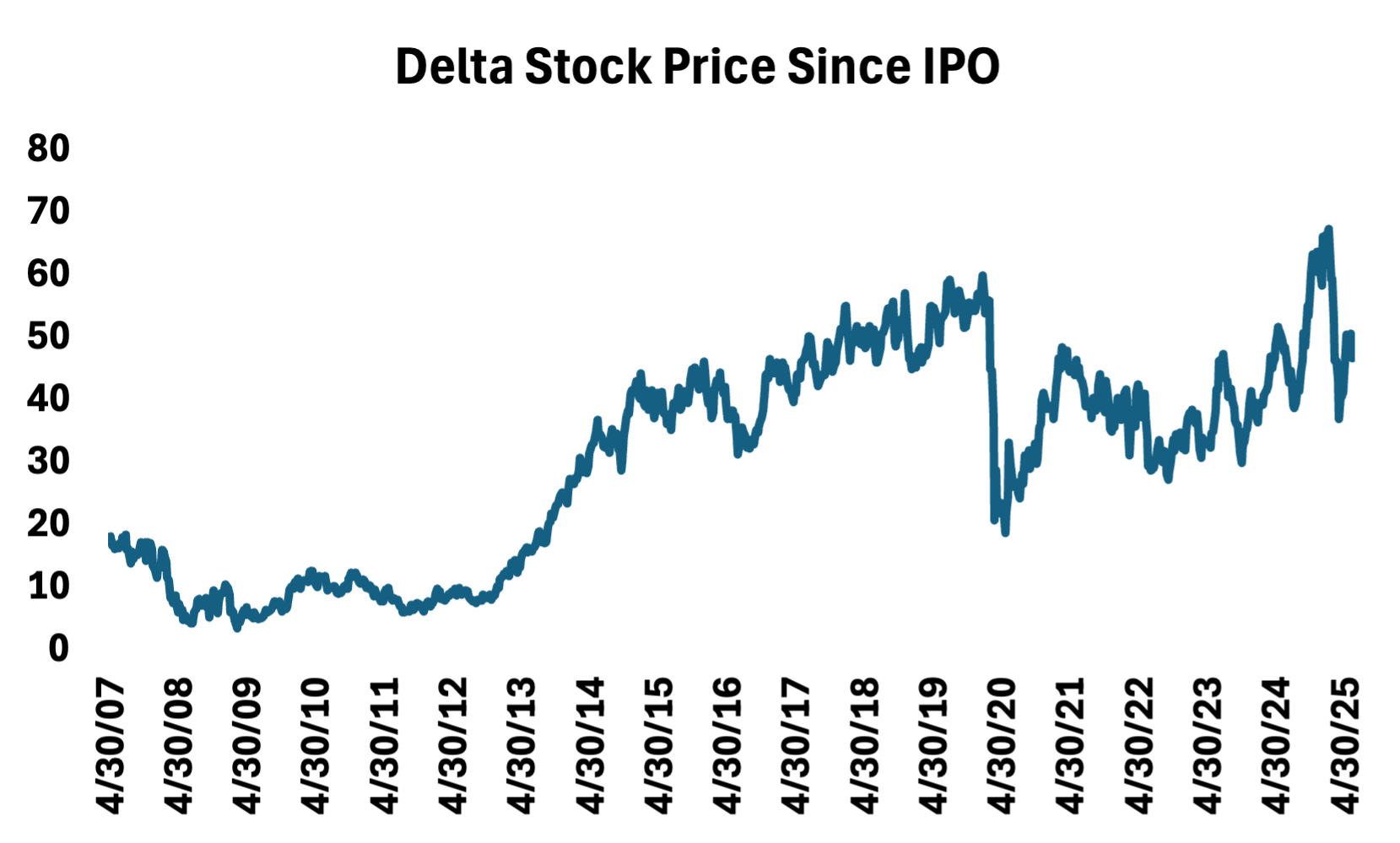

Using Delta to Illustrate Airlines' Vulnerability to Economic Shocks

Looking at Delta Air Lines' chart, the company has experienced periods of substantial losses in its stock since its IPO:

-

During COVID-19, Delta secured $3.8 billion in direct relief from the CARES Act and $1.6 billion in a low-interest government loan. Those who bought around the 2019 highs experienced a 68% loss from late 2019 to early 2020. While Delta's stock did recover by mid-2024, the recovery took roughly four years and required one of the strongest travel demand surges in history. Investors who held through the entire cycle merely broke even, while the S&P 500 gained over 80% during the same period.

-

More recently, at the beginning of 2025, Delta's CEO Ed Bastian made several public statements indicating it would be Delta's best year ever. However, governmental policy led to economic uncertainty, which forced Delta and other domestic airlines to pull their full-year guidance for 2025, causing a 49% drop from recent highs of $69 per share. This pattern reinforces the thesis: even during expansion periods, airlines remain vulnerable to sudden and severe drawdowns.

What Would Change This View

To be fair, there are scenarios where airlines could become more investable. Sustained capacity discipline, where carriers collectively limit seat growth to maintain pricing power, would be a meaningful shift. Continued industry consolidation that reduces the number of competitors could improve profitability structurally. And if carriers demonstrate an ability to maintain margins through a full economic cycle without government intervention, the bear case would weaken considerably. Until those conditions are met, the structural headwinds remain the dominant force.

Moral of the Story: Invest Your Money Elsewhere

With lower risk and higher historical returns, the S&P 500 offers a far more compelling investment opportunity than the airline industry. Airlines have struggled with high fixed costs and weak pricing power, resulting in razor-thin margins. To sustain operations, many carriers rely on elevated debt levels. During periods of economic uncertainty, not only do earnings decline, but the ability to service that debt is also threatened, raising the risk of financial distress or even bankruptcy.

Given these structural challenges, there is little justification for allocating long-term investment capital to this sector.

Equity Researcher · CFA Research Challenge Champion

Independent equity researcher focused on fundamental analysis and long-term value creation. Data-driven, fundamental-first.